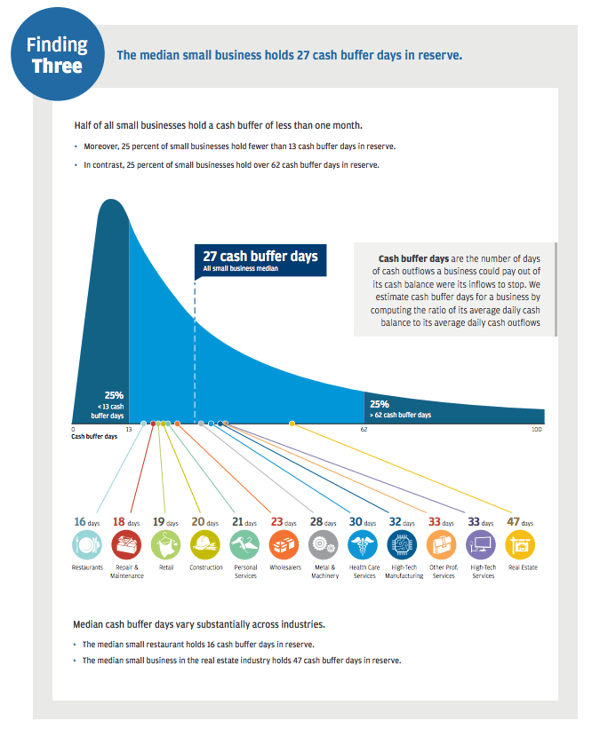

It is even shorter for some businesses (19 days for retailers, a mere 16 days for restaurants). That is not much time, and it should be a wake-up call to small business owners everywhere that how we save money is just as important as how we spend it.

The study, released by JPMorgan Chase Institute, reviewed the banking transactions of 597,000 small businesses who hold bank accounts with Chase in core metropolitan areas. The study sought to evaluate the ability of American small business owners to withstand negative economic shocks (such as a prolonged economic downturn).

Source: JPMorgan Chase Institute

Key Findings:

AVERAGE DAILY CASH BALANCES VARIES WIDELY

According to the study the average daily cash balance for all small businesses is $12,800. It is lower for repair/maintenance businesses ($5,800) and highest for high tech businesses ($34,200).

MOST BUSINESSES HAVE UNDER 30 DAYS' CASH RESERVES

On average small businesses have just 27 days of Cash Buffer (defined as the number of days a business could pay daily bills using available cash if all income were to stop).

CASH TIGHTEST FOR LABOR-INTENSIVE BUSINESSES

The more labor intensive the business the lower the Cash Buffer. High tech businesses have 38 days average Cash Buffer compared to only 18 days for Repair/Maintenance businesses.

Is Your Business Low On Cash?

There are steps you can take if you find your small business in a cash crunch:

Look at Big Picture - Is this a short term issue or a sign of bigger problem? If the cash crunch is due to the loss of one key customer contract, redoubling your sales efforts can help get you back on your feet quickly. If, however, there are larger issues going on (like a steady decline in customers over several months) then it may be time to re-evaluate your business model.

Get In The Weeds- Give a careful review of your income statement and look for where you can trim expenses for short or long term. Many times businesses sign up for a monthly service they no longer need, and simply neglect to stop the recurring credit card charges. All those charges quickly add up.

Consider a Short-Term Loan - If you have identified you have a short-term issue and you trimmed your expenses but find you are still short on cash, then a short-term loan may help. It is essential, however, that you carefully weigh the options first. A short-term loan will never solve a long-term problem (like fewer customers interested in your product). A responsible lender should be able to help you determine if a loan will help. Read our blog post here on how to determine if a short-term loan will help or hurt your business.